Hello,

Next data proved to be blow for investors who believe in the "guaranteed" by the government of 7.5% GDP growth this year. It turned out that both retail sales and industrial production in February was well below expectations.

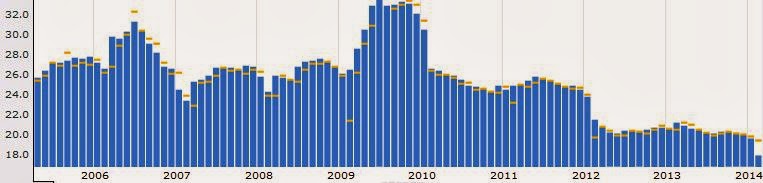

Retail sales y/y: actual: 11.8%; forecast: 13.5%; previous: 13.6%

|

| chart 1. retail sales in China m/m |

Fixed asset investment ytd/y: actual: 17.9%; forecast: 19.5%; previous: 19.6%

|

| chart 2. fixed asset investment m/m |

Interesting is, however, another statistic. In February of investment in urban areas rose by 17.9%. Looking through the prism of the developed economies, or even the majority of developing economies is insane tempo. However, the data were disappointing, as the market hoped for more than 19%. What's more, it shows that even at such a small slowdown in the sector of the economy the whole body gets out of breath.

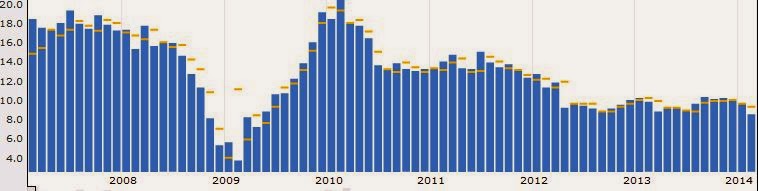

Industrial production y/y: actual: 8.6%; forecast: 9.5%, previous: 9.7%

|

| chart 3. industrial production m/m |

The weak data coming after earlier warnings from the export and PMI.

HSBC Final Manufacturing PMI: actual: 48.5% (below 50%, which means stagnation, no growth)

|

| chart 4. HSBC final manfacturing PMI m/m |

Investment in real estate sector for the last 12 months counted to February increased to a record 15.2% of GDP. So even to slow the economy, the structure of the whole economy has continued to deteriorate.

What does it mean?

If China actually have to change the structure of its growth, more serious slowdown is inevitable. Attempts slight tightening of monetary policy, which have a slightly cool down the real estate market, meant that the demand for them is lower than in the fourth quarter of last year, but the supply continues to grow. It seems, therefore, that if the demand is again not alive, the supply will have to adjust, causing a stronger inhibition of the total economy.

Besides official figures, appeared on the market about the subsequent problems of Chinese steel mills and aluminum. In addition, China's prime minister in an interview with European journalists admitted that many companies in China is facing a harder time, but the government will not save them, because they did not pose a threat to the entire financial system. From the perspective of the commodity market, this means one thing: a high probability of collapse of demand for industrial metals, the lower the growth rate of demand for energy resources and the lack of opportunities for stronger growth in demand for agricultural commodities.

On the markets, iron ore, steel, copper, aluminum, nickel, China represent more than 30% of global demand, and for more than 90% increase in demand in recent years.

Investment banks about Chinese growth:

Banks see growth in the Chinese economy in the first quarter at a level of 7 to 7.5%, it is 0.5 percentage points lower than in the series of data for February. Made the largest cut: BoA Merrill Lynch, lowering the forecast from 8% to 7.3%. At this level of growth also sees Nomura. HSBC predicts 7.5%, while SocGen "minimally above the 7%"

regards,

oscarjp

The information contained in this publication is not intended as an offer or solicitation for the purchase or sale of any financial instrument. Any opinion offered herein reflects oscarjp-chrimatistikos current judgment and may change without notice. Users acknowledge and agree to the fact that, by its very nature, any investment in shares, stock options and similar and assimilated products is characterised by a certain degree of uncertainty and that, consequently, any investment of this nature involves risks for which the user is solely responsible and liable.

No comments:

Post a Comment